From the collective design of a Balanced Scorecard to its abandonment: Organizational learning in question

- By Gérald Naro

- and Denis Travaillé

Pages 13 to 54

Cite this article

- NARO, Gérald

- and TRAVAILLÉ, Denis,

- Naro, Gérald.

- et al.

- Naro, G.

- and Travaillé, D.

https://doi.org/10.3917/cca.251.0013

Cite this article

- Naro, G.

- and Travaillé, D.

- Naro, Gérald.

- et al.

- NARO, Gérald

- and TRAVAILLÉ, Denis,

https://doi.org/10.3917/cca.251.0013

Introduction

1The last decades of the 20th century mark a turning point in management control research (Ittner and Larcker, 1998). In this context, the model of cybernetic regulation that has long been the paradigm underlying the philosophy of control (Hofstede, 1978), appears to be more and more discussed in favour of the learning model, judged to be more adapted to a competitive, dynamic and complex environment (Mevellec, 1990, Besson and Bouquin, 1991, Johnson, 1992, Lorino, 1995). So, since the 1990s, many publications highlight the role of management control systems in organizational learning (Argyris and Kaplan 1994; Simons 1995; Kloot 1997; Bollecker 2002; Chenhall 2005; Batac and Carassus, 2008, 2009; Dambrin and Löning, 2008). The model of control levers developed by Simons (1995) is particularly illustrative of this movement. It differentiates two control levers according to whether they intervene in the implementation phase or directly at the strategy formulation stage: diagnostic control levers based on cybernetic vision and simple-loop learning; the interactive control levers expected to favour emerging strategies (Mintzberg and al., 1998) and a double-loop learning (Argyris and Schön, 1978). The Simons model (1995) clearly poses the question of the role of management control systems in strategic and learning processes.

2In this perspective, the Balanced Scorecard (BSC) is a particularly interesting object of study in that it can be considered as much an interactive control lever as a diagnostic control lever (Malina and Selto, 2001; Tuomela, 2005; Kaplan, 2009; Kaplan and Norton, 2001b). According to Kaplan and Norton (1998), «Management processes built around the strategy articulated in the Balanced Scorecard must provide regular opportunities for double-loop learning—by collecting data about the strategy, testing the strategy, reflecting on whether the strategy is still appropriate in light of recent developments, and soliciting ideas throughout the organization about new strategic opportunities and directions» (Kaplan and Norton, 1996a, p. 252). In several publications, Kaplan and Norton (1996a, 1996b, 2001, 2009) consider therefore that the BSC can play a leading role in learning processes. However, even if their works are rich in examples of the BSC, they do not support this argumentation with an empirical demonstration. The purpose of this article is to study this very interesting question left open by the designers of the BSC: does the conception of a BSC within an organization generate learning processes? A longitudinal empirical study based on an intervention research carried out with two industrial companies makes several observations: during the conception of the BSC, the multiple interactions between the actors around the formulation of the strategy, the construction of the strategy map and the selection of the indicators, generated a triple process of knowledge acquisition, distribution of information and interpretation of information. Despite the abandonment of the BSC a few years after its creation, it appeared that the two companies had capitalized on the knowledge acquired during the design phases of the device. This observation offered us therefore the opportunity to question the organizational learning processes of the collective conception of a BSC and beyond its abandonment.

3The article is structured as follows: After presenting the conceptual framework and methodology of the study (1), we proceed to the analysis (2) and the discussion of the results (3).

1 – Conceptual and methodological framework of the research

4We present successively the conceptual framework (1.1) and the research methodology (1.2).

1.1 – The conceptual framework

5Several authors adopt a critical position vis-à-vis the BSC in which they criticize notably a static vision that can inhibit the strategy (Maisel 1992, Nørreklit 2000, Voelpel and al., 2006). Nørreklit (2000), in particular, states that even if Kaplan and Norton recommend that the BSC be a basis for double-loop learning, this does not seem to be clearly compatible with the highly hierarchical and mechanistic method they describe in their model. Nørreklit (2000) recommends then an interactive approach to the BSC: «the control processes should be more interactive during strategy formulation, during the building of the scorecard and during the subsequent implementation» (Nørreklit, 2000, p. 81). She backs up the work of Emmanuel and Otley (1995) in particular, who emphasize that, beyond a cybernetic approach to control, organizer of order and stability, a second pluralist approach represents control as emerging from the interaction of actors in the situation and promoting learning. For the authors, if we can consider these two approaches as conflicting, it is more useful to consider them as complementary. Here we find the complementarity and the interaction between diagnostic controls and interactive controls, represented by Simons through the image of Yin and Yang (Simons, 1995). As Simons (1995, p. 155) notes, this distinction between diagnostic and interactive control reflects two visions of the strategy: Diagnostic controls approach the strategy as a plan, while interactive systems consider the strategy as actionable models (strategy as patterns in action). The BSC invites us to rethink the strategy (1.1.1). By designing the strategy as actionable models, the BSC can become an organizational learning lever (1.1.2).

1.1.1 – Rethinking the strategy with the BSC

6Focusing on the role of the BSC in strategic processes leads to the study of the complex relationships that link control and strategy and form the basis of strategic management control. The historical case studies of Chandler (1962) and, in particular, his descriptions of the implementation of a «decentralization with coordinated control» at Dupont de Nemours and General Motors in the early twentieth century, have revealed that control is part of an organizational structure which, itself, stems from a strategy. The founding works of Anthony (1965) situate management control between strategic planning and execution control. Management control can then be defined as «a process by which managers ensure that resources are obtained and used effectively and efficiently in achieving organizational goals» (Anthony, 1965). Later, Anthony (1988) will deepen the strategic dimension of management control defining it as «a process by which managers influence other members of the organization to implement the strategies». Since then, this question of the interconnections between control and strategy has been studied and discussed. Without doubt this is because of its complexity and the many ambiguities it allows (see Bouquin 2000, Denis 2003). For Bouquin (2000), research has explored new dimensions of the relationship between control and strategy and, through this enrichment, they discovered the complexity of the issue. As a result of the limitations in Anthony’s typology, and based notably on the work of Simons (1995), Bouquin then sketches an interesting hypothesis:

“In the face of ‘introverted’ reactive management control, (Bouquin, 1986), of surveillance, the best known and unfortunately the most taught, there exists a proactive, extroverted management control, which is a key part of the strategic emergence process “.

8In the same perspective, Denis (2003) observes that it was from criticisms of the traditional approach to strategic management control that a renewed thought of strategic control developed, resulting in four different visions of roles played by control as part of its articulation with the strategy (Denis, 2003, p. 3). Four areas of questioning thus question the role of control in the deployment of the strategy, the alignment of the variables in coherence with the strategy to focus the strategies, the management of the changes and, the exercise of a managerial vigilance on the merits of the strategy. Denis then conforms with several authors (Schreyögg and Steinmann, 1987, Prebble, 1992) showing a «critical» approach with regard to strategic control:

“These authors believe that the primary function of strategic control is to submit the assumptions, objectives and plans of the organization to continual criticism and challenge. It is therefore necessary to develop a capacity to conduct double-loop learnings and continually test the relevance of the ‘staging’ in effect within the organization.

10These evolutions of the conceptions of the control of strategic management refer more fundamentally to a change of perspective in the representations of the strategy. Several studies (Mintzberg, 1994, Mintzberg and al., 1998) describe two visions of strategy: the strategy considered as a plan; the strategy envisioned as a model—a theory—of action or, in other words, as a hypothesis. In this latter approach, the strategy is no longer seen as an abstract black box and reified. Far from being a priori, it emerges at the end of a process of collective deliberation:

“The strategy is a set of hypotheses about causes and their effects. The BSC needs to clarify the relations or assumptions between the objectives (and the indicators) in several areas so that these objectives are validated and used to guide the actions”.

12The strategy map of the BSC then appears as an essential factor in the construction of the strategy. Although observing business practices reveals that the BSC is not always accompanied by a strategy map (Othman, 2006; Bukh and Malmi, 2005), in the Kaplan and Norton model, however, it appears to be consubstantial with the BSC. If, in the first version of the BSC, especially in the initial presentation given to us by Kaplan and Norton (1992) in their first article published in the Harvard Business Review, the BSC appears at first glance as a strategic dashboard structured in four axes. In subsequent publications (Kaplan and Norton, 1996a, 1996b, 2001a, 2001b, 2004, 2006, etc.), the strategy map will rapidly take centre stage in the model, to the point where the two initiators of the BSC will devote an article to it (Kaplan and Norton, 2000) and a book (Kaplan and Norton, 2004). As noted by several authors (Cobbold and Lawrie, 2003; Trebucq, 2011; Choffel and Meyssonnier, 2005), the BSC thus experienced several stages in its evolution to the point of going beyond the stage of a simple tool of control of management, to be established, at least in the publications of its designers, like a strategic management device and this, thanks in particular to its strategy map.

13The «cause-effect» model which structures the stratey map raises however several questions regarding its fundamentals. Researchers criticize Kaplan and Norton for the lack of clarity on the meaning they attach to the concept of causality (Nørreklit, 2000). However, Bukh and Malmi (2005) remind us that, according to Kaplan and Norton, the strategy map is primarily a hypothetical schema and not a model of relationships established. The strategy, as captured in the BSC «cause-effect» model, is more conjectural than generic. In fact, it represents the assumptions made by the top-management on «the best thing to do». Presented in this way, it is more in the managerial virtues of the BSC and in its capacity to create meaning for a collective of actors that we must look for its major contribution and not in any aptitude to verify causal relations a posteriori. As a model of representations and hypotheses about a strategy that does not appear as «engraved in stone», the contributions of the BSC lie more in its potentialities of double-loop learning (Argyris and Schön, 1978), than in simple correction loops with respect to pre-established objectives. Thus, as a model of hypotheses, the underlying representation of the strategy, as it is contained in the strategy map, refers to the theories of action developed by Argyris and Schön (1978) in their model of learning. It reflects guiding values and basic paradigms that can be constantly questioned. As noted by Kaplan and Norton (1996a), the BSC allows simultaneous learning in simple loop if the strategy is applied as intended and double-loop learning when determining whether the strategy remains viable and competitive. The BSC thus makes it possible to confirm or refute the assumptions made at the time of the formulation of the initial strategy (Kaplan and Norton, 1996a).

14Through its methodology, the BSC offers the opportunity for collective reflection on elements such as vision, mission, values or positioning. It thus provides a favourable framework for a process of collective construction of the strategy. In the same perspective, the collective conception of the strategy map and the causal relationships that structure it, the mechanisms of deliberation on the definition of objectives and the choice of indicators, can allow a collective of actors to interact and to gather together around a shared model of performance. The intersubjective communication process that emerges from these interactions can produce shared representations and stimulate organizational learning. The BSC can therefore be likened to a boundary object (Star and Griesemer, 1989) around which actors belonging to several social worlds (directors, functional managers, operational managers, etc.) interact, share representations and engage collectively in the construction of the strategy and a common performance model. By studying the deployment of the BSC in four entities of the same group, Hansen and Mouritsen (2005) show that the BSC is a boundary object in that it is sufficiently plastic to respond to specific contexts and organizational issues specific to each of the four cases, while maintaining its identity across different contexts of use. The authors reveal in particular that the BSC does not present itself as a predefined and normative model, but that the nature of the organizational problems specific to each studied unit explains the idiosyncratic nature of its use and the representations constructed by the actors. In the studied group, the strategic management control is the result of a learning process in which the BSC is an instrument for reformulating the strategy. This is no longer given a priori or simply admitted as a «black box» (Hansen and Mouritsen, 2005), but it is part of a reformulation by a group of actors. However, for such a process of collective construction of the strategy to work, the leaders must create favourable conditions. In particular, they must involve an enlarged group of subordinates in the experience of the BSC by stimulating dialogue and debate during the different phases of the design and deployment of the device. This interactive approach of the BSC can therefore be presented as a lever of organizational learning.

1.1.2 – The BSC, learning lever

15Organizational learning translates into collective learning and changes behaviour within the organization (Huber, 1991). In general, the issue of organizational learning refers to the acquisition processes and transformation of knowledge in the organization. It should be noted that these processes can occur at a triple, individual, group or organizational level. It is at the level of the organization in its overall strategic dimension that interests us in this study. Thus for Crossan and al. (1999, p. 522), organizational learning can be conceived as an essential means for achieving a strategic renewal of a business. This is thus how Kaplan and Norton (1998), see things when they use the Argyris and Schön model (1978) and are interested in the role of the BSC in double-loop learning. For Argyris and Schön (1978), organizational learning is the result of a process by which actors detect errors and act to correct them. It can be divided into two levels: adaptive learning in a single loop that produces minor changes in behaviour and does not result in significant change in values; the double-loop learning or generative learning that leads the organization to change the paradigm, which amounts to drastically revising the «theory of action» reflecting its guiding values and its founding paradigms. Figure 1 shows the model of learning defined by Argyris and Schön (1978) by locating the role that the BSC can play in the learning processes in single-loop and double-loop.

The role of the BSC in organizational learning processes

The role of the BSC in organizational learning processes

16As defined by Kaplan and Norton (2001a), the strategy can be considered as a model of hypotheses on cause-and-effect relationships. This translates into a strategy map which, based on the Argyris and Schön (1978) model, can be considered the organization’s «action theory». This «theory of action» refers to the basic paradigms and guiding values on which «action strategies» are based. A primary learning in simple loop, consists of when comparing goals and targets to results. In case of deviation, it is then necessary to make the necessary corrections. In the words of Kaplan and Norton (2001a), this involves achieving strategic alignment and «translating the strategy in actions» (Kaplan and Norton, 2001a, 2006). But a second type of learning, in «double-loop», consists of going back to the premises of the strategy (Schreyögg and Steinmann, 1987) by questioning the strategy map, that is to say the guiding values that form the basis of the «strategies in action» on which the objectives and targets of the BSC are defined. This would be more of a learning process of (re-) thinking strategy (strategic thinking) than a strategic alignment process. The way to consider the measurement or diagnosis of results, whether it be a purely cybernetic approach in the context of a diagnostic control or an interactive approach, seems essential here.

17As Kloot (1997) points out,

“The use of control devices such as feedback loops and budget discrepancies is designed to detect operational problems and the information provided by these control systems is used within common operational paradigms to correct operational problems. Hypotheses and policies are usually not questioned, resulting in simple loop or adaptive learning “.

19In contrast,

“Management control systems can also play a critical role in detecting and solving problems caused by environmental change, resulting in paradigmatic change (double-loop learning or generative learning)“.

21In particular, the transition from adaptive learning to generative learning requires a collective effort within the organization that can be stimulated by interactive control levers in the sense of Simons (1995). Thus, the BSC mobilized in an interactive approach, could foster generative learning when the strategy map is the product of interactive exchanges between members of the organization. Under these circumstances, learning can be described as organizational insofar as the construction process of the BSC leads to the transfer of knowledge and information between individuals or groups of individuals. It is therefore necessary to construct a shared representation of the strategy and the underlying assumptions that are at the foundation of its performance model.

22In this generative process, individual learning is no longer sufficient. It is therefore necessary to better understand how teams learn and how to create structures and networks to share learning experiences within organizations (Marquardt and Reynolds, 1994). Several authors describe organizational learning through four sets of constructs and processes (Levitt and March 1988, Huber 1991, Kloot 1997): the acquisition and distribution of knowledge in which information from multiple sources is shared, leading to new information and understanding (Huber, 1991, p. 90); interpretation, defined as «the process by which information takes on meaning or as the process of translating events and developing an understanding and shared conceptual schemas» (Daft and Weick, 1984, p. 294-296); organizational memory, the process by which knowledge is stored for future use, involving the accumulation and maintenance of organizational experiences (Kloot, 1997, p. 57). Huber (1991) details these constructs and the sub-processes by which they proceed (Fig. 2).

Constructs and processes associated with organizational learning

| Constructs and process | Sub-Constructs et Sub-Processes | Sub-Constructs et Sub-Processes |

|---|---|---|

| 1.0 Acquisition of knowledge | 1.1 Congenital learning | |

| 1.2 Experimental learning | 1.2.1 Organizational experiments | |

| 1.2.2 Organizational auto-appreciation | ||

| 1.2.3 Experimental organizations | ||

| 1.2.4 Non-intentional et non- systematic learning | ||

| 1.2.5 Learning curve | ||

| 1.3 Proxy Learning | ||

| 1.4 Graft | ||

| 1.5 Research and attention | 1.5.1 Scanning | |

| 1.5.2 Targeted research | ||

| 1.5.3 Monitoring performance | ||

| 2.0 Distribution of knowledge | ||

| 3.0 Interpretation of information | 3.1 Cognitive map and framing | |

| 3.2 Richness of the media | ||

| 3.3 Information overload | ||

| 3.4 Unlearning | ||

| 4.0 Organizational memory | 4.1 Storage and retrieval of information | |

| 4.2 Computerized organizational memory |

Constructs and processes associated with organizational learning

23Huber’s (1991) model captures the knowledge production and transformation processes that underlie organizational learning. In the same perspective, several conceptual frameworks have come to illuminate these learning processes. The framework proposed by Crossan and al. (1999), or 4I’s model, distinguishes four processes: intuition, interpretation, integration and institutionalization. But it is mainly the knowledge conversion model (Nonaka, 1994; Nonaka and Takeuchi, 1997) which provides a particularly enlightening vision for knowledge management. At the heart of the model, the interrelationships between tacit knowledge and explicit knowledge over interactions between individuals are crucial for the formation of new knowledge (Nonaka, 1994, p. 15). The conversion of knowledge proceeds from four dynamic processes: socialization, externalization, combination and internalization. If the knowledge conversion model thus offers particularly fertile research perspectives for management control (Bollecker, 2002), we deliberately delimited our conceptual framework to the double-loop learning model developed by Argyris and Schön (1978), enriched and deepened by the notion of generative learning developed in the work of Huber (1991) and Kloot (1997). At the heart of the research programme that guided this longitudinal study, we wanted to delve deeper into a very interesting question, advanced but nevertheless little documented by Kaplan and Norton: that of the role of the BSC in the process of learning in double-loop. That is why we focused on this concept. Huber’s (1991) model allowed us to enter the «black box» of double-loop learning to observe in a more operational way the processes of acquisition, distribution, interpretation and memorization of knowledge, related to the design of a BSC.

24The design of the BSC, using an interactive approach can thus favour acquisition and distribution processes. This could involve, in particular, experimental learning sub-processes, in which the actors of the organization analyze return on cause-effect relationships formulated as assumptions in the strategy map. As noted by Huber (1991, p. 91), «an approach to fostering organizational learning is to increase the accuracy of feedback on cause and effect relationships between actions and results». Another aims to ensure the collection and analysis of these feedbacks. Huber (1991, p. 92) notes that a self-appreciation based on the interaction and participation of the members of the organization can also foster the acquisition of knowledge and thus organizational learning. He also emphasizes the importance of performance monitoring. The BSC may also generate interpretive processes, particularly in the context of construction of the strategy during which the actors develop a collective representation around a shared model of a strategy map and the definition of the constructs, giving rise to measures of performance. Finally, the strategy map of the BSC, could therefore constitute the cognitive map and the conceptual framework on which a shared performance model is based. In doing so, they build meaning, develop a translation process and produce a shared understanding and common schema conceptualizations (see Daft and Weick, 1984, pp. 294-296, cited by Huber, 1991, p. 102). For Kaplan and Norton (1996a), the BSC then appears as a representation of the shared vision of the strategy. The design of the BSC and, in particular, the collective formalization of the strategy map and its materialization in the form of objectives and measures, such as the recurrent use of the BSC during interactive piloting, would allow the construction of an organizational memory. As specified by Simons (1995), interactive control processes are by definition collective and can thus foster the emergence of generative learning stimulated by dialogue and debate. But, if the use of the BSC as an interactive piloting tool has already been subject to analyses and descriptions, a minority of research is focused on the learning processes that emerged during the design phase of the BSC. So it is precisely to this privileged moment of building meaning and collective learning that our research pays special attention. For Kloot (1997), the learning processes generated during the design phase of management control systems are crucial to accompany change and ensure the survival of the organization. The observation in our two case studies of the abandonment of the BSC a few years after its conception for example, provided us with an opportunity to observe to what extent the learnings developed during the design of the BSC could subsist and incarnate in practices and the implementation of new tools.

1.2 – The methodology

25The methodology uses a processual approach based on intervention research (1.2.1) and a longitudinal study of two business cases (1.2.2).

1.2.1 – A processual approach based on intervention research

26Studying the role of the BSC in strategic and learning processes requires a dynamic observation approach. The mobilized methodology is part of a processual approach consisting of describing, analyzing and explaining the what, the why and the how a sequence of individual actions, all based on the assumption that social reality is not a stable condition, but instead is a dynamic process (Pettigrew, 1997). We adopt a processual approach in order to understand the dynamic interrelations between control (controlling) processes and strategic (strategizing) processes (Chapman 2005, Jørgensen and Messner 2009). For researchers who fit into this movement (Hinings, 1997; Pettigrew, 1997), qualitative methodologies and longitudinal case studies seem particularly appropriate. In this perspective, we adopt a methodology in which researchers interact with their field, within the framework of the transformative intervention research. While this type of approach has long been relatively rare in management control research (Kasanen and al., 1993), it seems that this has evolved today with the development of action research such as «innovation action research» (Kaplan, 1998) or «constructive research approach» (Kasanen and al., 1993, Labro and Tuomela, 2003). Our research is particularly relevant to innovation action research (IAR) which consists, according to Kaplan (1998), of developing a methodology for action research involving the participation of researchers in managerial innovations through their field experimentation, which should lead to the development of new theories and practices. Kaplan (1998) then refers to his work with Norton on the BSC. In the IAR, researchers develop and refine the theory of a new managerial practice that is expected to be broadly applicable to a wide variety of organizations (Labro and Tuomela, 2003). Through our study, we wish to develop our understanding of a pre- existing management control tool—the BSC—to study its role in organizational learning processes. Doing so, our research is part of a project of knowledge little explored by Kaplan and Norton. It is a step in a longitudinal research programme carried out in two industrial enterprises over a period of about 12 years for one company and 8 years for the other. The research program aimed to provide answers to three sets of complementary questions: the role of the BSC in the design of the strategy; the control levers mobilized in the design and use of the BSC and, more specifically, the modalities and effects of an interactive BSC approach; the role of the BSC in organizational learning processes. Several publications have been produced on the first two themes. This article more particularly develops the third.

1.2.2 – Longitudinal study of two cases of industrial companies

27We conducted a longitudinal study on two cases of companies in which we initially conducted an intervention research. These two companies were selected for three reasons: firstly, their industrial activity, which allowed identifying the physical processes of value creation. Secondly, these two companies are of intermediate size which allowed us to grasp the strategic and operational levels. Thirdly, these production units were chosen because of the strong involvement of their management teams in the research project. Very interested in the integrated and multidimensional nature of the BSC, the leaders of the two companies were willing to commit the necessary means to the implementation of the device. For reasons of confidentiality, the two cases have been renamed AMIDON and MECATRONIC. AMIDON, which employs 200 people, is a profit centre of an international group in the carton packaging sector; MECATRONIC is a SME independent of the sector of precision mechanics. It has 130 employees.

28Both companies had similar aspects in many respects. In both companies, a participative management style was adopted with the intention of involving a large group of employees in the management of the organization. The CEOs of both companies also seemed to be driven by an entrepreneurial vision and eager to develop strategic thinking around a collective project. All the conditions seemed to be there to allow us to observe how the design of a BSC can play a role in forming a strategy. In both cases, the experiment responded to the need for a new joint project able to (re) mobilize a collective.

29The research method took the form of an active participation of researchers in the development of the BSC in close cooperation with the management teams extended to a set of collaborators at intermediate and operational levels. At every stage, interviews were used to collect stakeholder representations and regular observations were made each year.

30However, once the BSC reached an operational stage, the two companies did not wish to continue the intervention research experiment. At AMIDON, following its absorption by a competing group, the Chief Executive Officer left the company and his replacement did not wish to extend the experience, especially because the device was not part of the management tools of the group. At MECATRONIC, the company has suffered a severe crisis and a large part of the direction has been renewed. In both cases, although the research intervention experiment was terminated after the design phase of the BSC, however, the companies accepted that the researchers continue their research work as observers. If it was observed that the BSC had not passed the stage of its routine implementation in the form of a steering system, this observation established in the two companies, reinforced us in the idea that it was interesting to deepen our analyses and to continue our observations in order to study the learnings that could remain after the abandonment of the BSC.

31The AMIDON study was conducted over a 12-year period and the MECATRONIC study was conducted over a period of 8 years. The investigation method is part of a longitudinal approach structured in two phases: a phase of immersion and intervention; a phase of observation and distancing.

An immersion and intervention phase

32This phase took place between 2001 and 2003 at AMIDON and between 2005 and 2006 at MECATRONIC. During this stage, the researchers interacted with the main actors of the two companies and conducted an intervention research consisting in formalizing the strategy and building a BSC. The methodology for formalizing the strategy was conducted during several working meetings with stakeholders to clarify the strategy. The design methodology of the BSC proceeded slightly differently in both companies. At AMIDON, work meetings were organized by processes to determine their objectives, their key success factors, the action variables and the performance indicators. The definition of processes has derived from mapping established as part of a certification process. The actors in each process had to coordinate with those of other processes. The objective was initially to build process dashboards. Meetings were then organized on an expanded steering committee to synthesize these dashboards to build the strategic map and the BSC. At MECATRONIC, the role of the researchers was also to facilitate several work meetings with the actors. Other meetings were also organized in the absence of the researchers. For example, after explaining the purposes and methodology of the BSC and leading a strategic seminar, the researchers allowed the actors in a first step to build collectively their strategy map, then in a second step, proceed to the definition of the indicators. At the end of each of these two stages, a pooling took place with the researchers, before proceeding to the next stage.

A phase of observation and distancing

33After completion of the construction phase of the BSC (2003 at AMIDON, 2006 at MECATRONIC), semi-structured interviews were conducted once a year in each of the two companies in order to study the practices adopted in the use of the BSC.

34It was particularly important to observe how it was used as a diagnostic or interactive control lever. Most importantly, we wanted to understand its role in strategic processes and learning mechanisms. So, at AMIDON, once a year between 2004 and 2007 we interviewed several actors: the General Manager, the Management Controller, the Sales Manager and the Production Manager. At MECATRONIC, between 2007 and 2009, we interviewed the General Manager and the Director of Sales and Purchasing (Business Manager). Then, between 2011 and 2014, we interviewed the Management Controller, the Quality Manager and a Workshop Supervisor at AMIDON, while at MECATRONIC the General Manager and his second in command, the Business Manager were interviewed. The choice of the various interviewees is explained by the fact that over the period, the acquisition of AMIDON by a competing group and the restructuring of MECATRONIC following significant economic difficulties, led to a strong turnover among the Managers in place. Most of the management teams were for the greater part renewed in both companies.

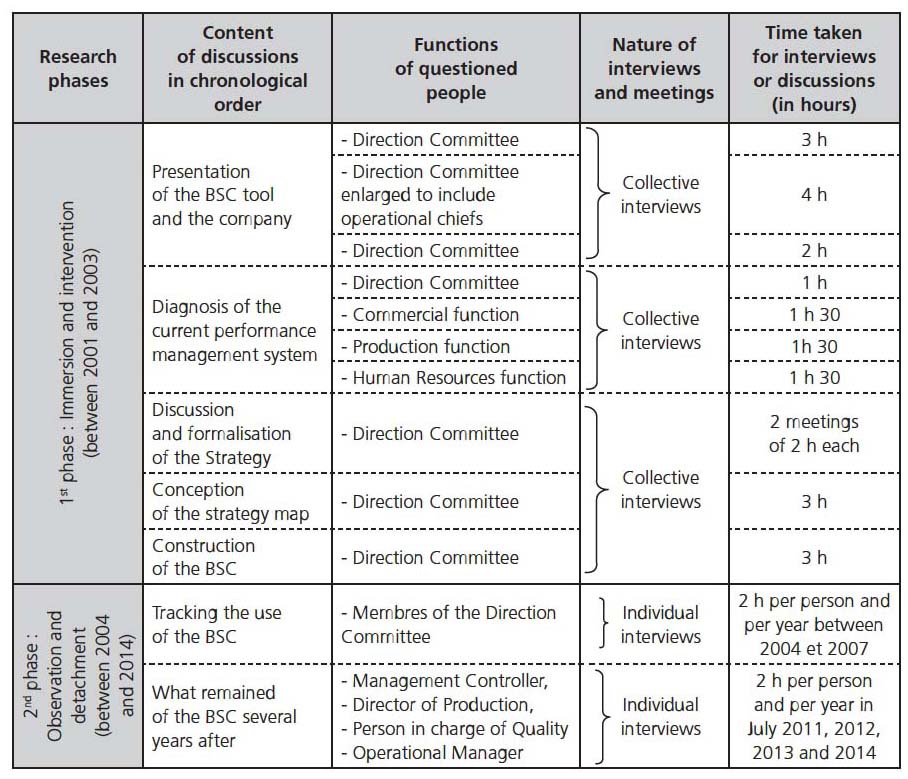

35In the appendix, the frame of the interview guides used during the two phases of the research (immersion and intervention, observation and distancing) is presented. We proceeded with a manual coding in two stages: an open coding (Strauss and Corbin, 1998) at first. This allowed us to highlight more key themes related to the different stakeholders’ view of the contributions and limitations of the BSC experience, the lessons they gained from it, the different stages of the process learning and knowledge, etc. Secondly, we carried out an axial coding (Strauss and Corbin, 1998), which enabled us to reveal elements of response with respect to our questions of research by intertwining the different themes highlighted. In addition to the various semi-structured interviews conducted with managers of both companies, it should also be noted that these two entities recruit trainees or apprentices with a Master’s Degree in Management Control each year. Researchers associated with the project, members of the Master’s teaching team, have access to continuous monitoring of the two organizations, on the occasion of learning visits, thesis supervision and defense. Tables 1 and 2 summarize the list of meetings and interviews conducted at AMIDON and MECATRONIC.

List of meetings and interviews carried out at AMIDON

List of meetings and interviews carried out at AMIDON

List of meetings and interviews carried out at MECATRONIC

List of meetings and interviews carried out at MECATRONIC

2 – Results

36The results of the two case studies initially revealed that an interactive approach to the BSC during its design phase led to an organizational learning process consisting of three mechanisms: knowledge acquisition, distribution information and interpretation (2.1.). Yet, unexpectedly, they also showed the abandonment of the BSC. Despite this abandonment, it was interesting to study what remained of the BSC several years after its conception in order to identify learning born from experience. The observations then showed a capitalization of experience (2.2.).

2.1 – The design of the BSC and the learning observed in the two case studies

2.1.1 – The design of the BSC at AMIDON

37The organizational context facilitated the implementation of the BSC project within the AMIDON plant. The commitment of the site management was paramount to the BSC design project. From the start of the project it was open to all forms of innovation and led to an inter-service dialogue. For the site director, this management approach should represent «an investment for the future», while specifying: «the return on investment not being necessarily measurable in the short term». The management found it necessary to communicate to facilitate the implementation of the project but also to make it survive. At the start of the project, the plant had an environment conducive to the integration of projects and this infatuation has undoubtedly played a large role in the emergence of a collective learning approach. All the people interviewed were very sensitive to the arguments generally accepted in favour of the BSC: the BSC is not only interested in financial indicators. It is also interested in more qualitative indicators such as customer or staff satisfaction. The BSC is therefore based on a global approach to business, a multidimensional performance; the BSC is part of a long-term value of the company by including indicators focusing on intangible aspects such as innovation and learning.

38The members of the BSC project started with one observation: on the one hand, all the dashboards used by the plant before the BSC project combined only result indicators that favoured the financial aspect; on the other hand, these indicators of delayed performance only allowed us to apprehend the effects of actions already undertaken by taking stock of past performance. But the leaders were getting the results they were subjected to.

39With the BSC project, management wanted to gain a more holistic view of performance and not be content with financial data. Several meetings organized by working groups, involving the management team and several process managers, made it possible to identify key success factors to access the strategic vision. Their identification was completed with the design of the strategy map. The work was based in particular on a mapping of the processes established in the framework of certification. Each process resulted in a collective definition of the missions, conditions of success, action variables, indicators and finally a process dashboard. The working group then asked about the upstream factors that influenced outcome indicators. This led to the creation of a strategy map based on the four axes advocated by Kaplan and Norton. Its design then made it possible to highlight the key elements of management of the AMIDON site and to create a dynamic of continuous improvement of the process of value creation. Figures 3 and 4 describe the strategy map and the indicators selected in the AMIDON BSC.

The strategy map of the BSC at AMIDON

The strategy map of the BSC at AMIDON

AMIDON’s BSC

AMIDON’s BSC

40The BSC approach, which has since been geared towards a long-term promotion of the company, has made it possible to clarify the strategy which was then turned towards customer satisfaction and to translate it into concrete actions that everyone can understand. Thus, the local objectives of managers were coordinated with the strategic objectives defined by management. All processes have been questioned in a similar way. Finally, existing dashboards have been improved and other control systems have been introduced.

41We must emphasize here the importance of the interactive dimension of the project which is above all a collective work, “a human adventure” according to the director of the site:

“The project demands a desire for transparency and cooperation; It improves internal communication, creates a dialogue between previously compartmentalized services and reduces the phenomenon of information retention. There is indeed strong territorial logic in French companies and the Gallargues factory is no exception to this rule: lack of cooperation between the different services, retention of information to continue to preserve some power. The BSC breaks down these barriers and serves as an instrument of mediation between the actors: the interservices meetings give the possibility to each department to expose the constraints that it faces. The debates give them an opportunity to work together toward a common goal: the performance of the site.”

43The discussions, however, highlighted contradictions in terms of steering. The interactive dimension of the approach has led to initiatives that would not have been perceived without this approach and to create value added for the client.

“I am asked to buy the cheapest pallets possible to optimize the cost, but the shipping department and customers ask for quality pallets to be able to move them easily.”

45The BSC project was a real success during its creation phase but it quickly ran out of steam and finally was abandoned a few years later. This experience, however, marked the management of the organization and allowed its control tools to be improved.

2.1.2 – The design of the BSC at MECATRONIC

46At MECATRONIC, the BSC project was part of a change of management perspective.

The design of the BSC thus coincided with the desire of the managers to introduce a participative management with more active involvement of the Heads of Lines in the strategic axes of the company. The idea was to stimulate their ability to take responsibilities and autonomy, while waiting for more initiatives, responsiveness and risk-taking. Their participation in the Management Committee was also intended to facilitate transversal exchanges and knowledge transfers between Line Managers and the Board of Directors as well as between Line Managers. At the instigation of the Director General, strategic thinking was thus set up within the enlarged Management Board and continued with the design of a BSC. Key success factors were identified collectively. In the same way, the design of the strategy map and the choice of indicators were made in the context of several meetings coordinated by the researchers, bringing together Directors, the other members of the Board of Directors and the Heads of Lines. Figure 5 and Table 3 present respectively the strategic map and the elements of the BSC developed collectively by the actors of MECATRONIC.“I wanted to use the BSC as a tool for change.”

The strategy map of MECATRONIC

The strategy map of MECATRONIC

The elements of the MECATRONIC BSC

| AXES | OBJECTIVES | INDICATORS |

|---|---|---|

| SHAREHOLDERS |

|

|

| CLIENTS |

|

|

| INTERNAL PROCESSES |

|

|

| LEARNING – INNOVATION |

|

|

The elements of the MECATRONIC BSC

2.1.3 – A design phase rich in learning

47In both companies, the collective reflection of the actors to build the strategy, formalize it with a strategy map and finally define the BSC, seems to have played a positive role in organizational learning. In particular, the BSC enabled actors from different sectors to interact around the same theme. Actors from different functions and different skill levels and representations gathered around the design of the BSC. Three of the four foundations of organizational learning (Huber, 1991) were found: knowledge acquisition, information distribution, and information interpretation.

Acquiring knowledge

48At AMIDON, before the BSC project, the plant was part of a dynamic approach largely influenced by the personality of its leader who did not hesitate to invest in intangible capital. This dynamic of research for innovation was reinforced by the company’s commitment to a quality management policy through ISO 9001 certification. This ISO 9001 project allowed the plant to describe all its activity as a process and to receive the regional quality prize in 2001. Shortly after the implementation of this approach, the researchers came to present their BSC project to AMIDON’s management. The Director of AMIDON, looking for a new project to boost his business accepted the launch of the BSC project in his unit. The project then started with training sessions for senior staff in strategic analysis and the BSC, led by the researchers. The leaders then trained their subordinates so that the BSC tool be known to all AMIDON staff.

49At MECATRONIC, only the two head managers had a real knowledge of the principal concepts of strategic management. Several years earlier, the CEO had attended a strategy seminar. But above all, the Business Manager, had recently completed an MBA programme at a management school. He attended a BSC course and chose to complete his MBA thesis on this topic. With the help of the researchers, he convinced the CEO to experiment with the BSC in the company. The other members of the Executive Committee had little or no knowledge of the strategic analysis. As for the line leaders, their knowledge was essentially operational knowledge. The first sessions of the experiment were thus devoted to a presentation by the researchers of the BSC and its methodology.

50Among the knowledge acquisition subprocesses involved in both cases we note particularly an experimental learning, fitting precisely in line with the processes generated by the design of the BSC. Here indeed, the design of the strategy map, through the identification of cause and effect relationships, the definition of objectives and constructs and their measurement in the form of indicators, has created a common knowledge of the company, its strategy and key performance factors. Now, a fundamental role was played by the participatory nature of the BSC design method and the interactions between actors that underpin it. This is in line with Huber’s (1991, p. 92) observations on the determining role of collective and interactive self-appreciation subprocesses.

Distribution of information

51At AMIDON, the BSC project has enabled the actors of different functions to work together. For example, the multifunctional nature of process groups has allowed them to be aware of the needs and means of other functions. The research of collective solutions have thus solved the problems which has had a favourable impact on the decompartmentalization of the services of the company. Ambiguities have been removed and synergies have emerged. For example, it became clear that different duties were identical tasks for the management of their activity. As a result, knowledge and tools could then be shared to avoid redundancy in everyone’s work. The systematic enumeration of ideas during meetings contributed to the knowledge of good practices and their dissemination within the organization. The objectives were then sought, initially with good practices, and their respect to verify if the targeted performance was achieved:

“The good practices constitute a real anticipation (…) as they are upstream of the result, I am able to influence my result by acting on them”.

53Finally, because goals, actions and indicators have been built and implemented collectively, it has become more logical to work together to achieve these goals. This approach has been innovative because, previously, each manager worked only with his own tools to maximize his performance without necessarily having the means to act. Here, the interaction between the different services has been strengthened because everyone has been aware of the multi-responsibility for performance. Thus, when a significant variation appeared to be unfavourable, the managers concerned met and a collective solution was sought.

54At MECATRONIC, a greater interest in the experiment was shown with the process of change that it entailed for the company:

“This has resulted in a learning tool that enables the strategy to be explained and to involve all the company’s stakeholders in a common strategic vision”.

56The various working sessions made it possible to question the strategy.

57The Line Leaders emphasized the learning role of the BSC and ensured that they understood more clearly the strategic directions of the company that resulted. This remark suggests that they felt more involved in the company’s strategy:

“We feel more involved. It’s good to know where we are going and why. That puts things in place. The strategy, if not implemented properly can be confusing! Things do not make sense anymore”.

«Previously, there appeared a series of events. It’s better to incorporate strategic decisions at the same level».

60Two of these actors affirmed that they played a role and that they influenced through their remarks, the vision and the direction of the leaders:

“They had their ideas, we managed to change their minds”.

«There are things that came directly during the work—for example, during the discussions on certain families of products or our proposals to make complete kits».

Interpretation of information

63To define interpretation, Huber (1991, p. 102) draws on the work of Daft and Weick (1984): «Interpretation can be defined as the process by which information makes sense (Daft and Weick, 1984, p. 294), and also as the process of translation of events and development of shared understandings and conceptual schemas» (Daft and Weick, 1984, p. 286). In both case studies, it appears that the finalization of the collective design stages of the two strategy maps and the selection of performance indicators, helped to build a shared vision, formalized in the form of documents presenting the two strategy maps. In both cases, at the end of the design phases of the strategy map and the selection of the indicators, the actors gave meaning to different concepts and hypotheses, which they translated in the form of objectives, sequences of causality and indicators of performance. A very interesting example is provided when AMIDON designed the strategy map, through this exchange initiated between the Director of Production and the Director of Commercial Function, on issues related to the mission and the business professions:

“Our mission is to provide our customers with cardboard packaging at the best value for money while respecting their deadlines. This means controlling costs, time and quality better than our competitors.”

«I would say that our mission is first to identify the needs of customers to offer them customized, innovative and comprehensive solutions for cardboard packaging. That is, that which integrates both the constraints of the customer into terms of logistics, transport, storage, but also packaging and merchandizing of their products».

«Yes, that’s it: to fully understand the needs of our customers, and then offer them global and innovative solutions for cardboard packaging that meet their needs. It’s up to us to adapt our processes in order to be competitive on our costs, our delivery times and the quality of our products. That’s where we make the difference».

67Through their interactions, the actors have thus arrived at a performance model corresponding to a shared representation, formalized by a strategy map and indicators, understandable by all and adopted as a common frame of reference. For Huber (1991, p. 102), among the subprocesses that favour interpretation and, by extension, organizational learning, the existence of a common cognitive map, as well as the communicated conceptual framework, play a vital role. In both cases studied, the BSC constituted a process of construction of collective representations. As seen previously, the interest of the BSC lies in its learning virtues, especially during the development of the strategy map and managerial processes. which allow it to be set up during its design phases. We also question these two cases concerning the relevance of the strategy map which seems very simplistic. Its linear representation seems to misrepresent the complexity of the causalities leading actors to a biased interpretation of strategy and the performance model. Nevertheless, such a simplification allows for a sharing of representations which offers opportunities for hierarchical and transversal exchanges and provides a framework for reference to the action. In addition, our cases provide an unexpected result: the BSC was able to provide a formalized model of performance that, when it gives rise to informal discussions, makes possible a better interpretation of the complexity of the strategy. The framework defined by the strategy map in the two case studies would constitute a common reference model: a meeting with discussions between the managers could be structured, making it possible to change the strategic representations. It seems then possible to question the interest of the BSC as a boundary object (Star and Griesemer, 1989). Indeed, at the beginning of the experiment, all the actors did not share the same vision. In both companies, the production function oriented towards the search for productivity was difficult to organize in response to the urgencies imposed by the commercial function and the general management. During the construction of the strategy map, through their interactions, the actors managed to highlight their contradictions, which were then debated. During these exchanges, the search for the key factors of success led the actors to seek compromises consistent with the competitive requirements of the company. In both cases, the customer focus has driven all functions to come together around a common vision.

68Finally, during the design of the BSC, processes of knowledge acquisition, information distribution and interpretation were born. It was therefore interesting to study how the learning processes at work during the BSC design spawned organizational memory. This fourth foundation of organizational learning (Huber, 1991, p. 90; Kloot, 1997, p. 57) describes the processes by which knowledge is stored for future use. involving the accumulation and maintenance of organizational experiences. To analyze these processes, it seemed important to us to study, several years after its conception, the evolution of the BSC in the two companies.

2.2 – Capitalization of knowledge despite the abandonment of the BSC

69During these years, the researchers regularly asked the main actors about the evolutions and the learnings emanating from the experience. A first observation quickly emerged: in both companies, the BSC experience did not go beyond the model design; we found an abandonment of the BSC (2.2.1). Strategy maps and performance indicators had not been translated into practice by regular use of the BSC in the form of steering by dashboards. We can draw several lessons on the favourable factors and obstacles to learning (2.2.2). Despite the abandonment of the BSC, several elements still persist in both companies where we have observed a capitalization of learning born from experience. In particular, we observed a memorization of the knowledge acquired during the design of the BSC (2.2.3).

2.2.1 – The finding of abandonment of the BSC in both companies

70In both cases, the BSC experience did not go beyond the stage of designing strategy maps and defining performance indicators. In concrete terms, during the semi-structured interviews conducted in companies during the years following the BSC experiment, the researchers were unable to observe any diagnostic or interactive use of the BSC in the form of scorecards or dashboards. It is now important to consider the reasons and modalities of this abandonment of the BSC in both case studies.

AMIDON

71Following the upheaval of the organizational context and particularly with the reinforcement of the shareholder pressure, the BSC was abandoned. This failure illustrates the limitations of the BSC, denouncing its normative dimension and the fact that it does not take into account the specificities of the company.

72Following a merger of the group owning the AMIDON factory with another group, the new group adopted an international vision and was introduced a few months later on the stock market. Therefore, the stakes are not the same anymore. Priority is no longer to be profitable by creating added value for customers. The company must now create shareholder value and take a short-term view of performance. We move from a human-scale factory to a group logic oriented towards the creation of shareholder value. The factories are more closely monitored by headquarters with the help of binding financial reporting and this policy change is felt by decision-makers:

“The group has imposed a harmonization of information and reporting systems (…) Reporting systems have taken precedence over local piloting initiatives as developed, for example, at AMIDON”.

«We have vision problems to pilot, no vision of the future (…) I wonder if I will not give up my own tables and if I will work directly on the reporting tools. The data is entered into a primary working tool most of the time in the form of Excel tables and the results are copied into the reporting tool to be analyzed by headquarters. This double entry represents a significant cost in terms of time».

«I lost my autonomy in my management choices».

«The reporting and actions imposed by the group takeover (…) my tasks are now focused around reporting, the budget process and the justification of budget deviations; I have less time to perform one-off missions».

77All sectors of the compagy should adapt their working methods to the expectations of the group. The BSC no longer fits into this new policy.

«The BSC is a complementary tool; it cannot replace the reporting or the budget. It is a time- consuming tool. We must make choices».

«The Balanced Scorecard approach was not yet anchored in work habits».

80As a result, the BSC is running out of steam, indicators are no longer updated due to lack of time and motivation. The BSC imposes in effect the search for more qualitative information and is therefore more difficult to collect. Everyone is going back to their own proper tables.

81This alteration of the environment did not give the tool a chance. The departure of the general manager of the AMIDON factory, initiator of the BSC project, also played an important role in the abandonment of the project. Investment in intangible assets have been gradually abandoned, the return on investment must be measurable in the short term (two years). Innovation projects, especially managerial projects, no longer fit within the organization. To keep a tool like the BSC functioning it is important to communicate. It is often easier to motivate individuals during the presentation and dialogue phases than to sustain the instrument over time.

82The BSC project represents a cost for the company especially in terms of time. The BSC advocates a multidimensional vision of performance and tries to meet all the needs of the company in the same way. However, every decision-maker in the company has different needs: for example, the Production Manager and CFO do not have the same needs or concerns:

“I want to know the status of my stock every day, the productivity of my machines and my workforce, the tracking of orders. My goal is to better adjust my human and material resources to the volume of orders”.

«I need a monthly follow-up, I want to know the costs. The data, the periodicity are important, each business section of the company has different needs».

85Following the abandonment of the BSC, in parallel with the reinforcement of an omnipresent reporting, we note the evolution of management control of AMIDON towards more operational dashboards. To meet the expectations of the group and in particular the pressure of the reporting imposed by the headquarters, the controllers have opted for dashboards facilitating the financial aspect and responsiveness. Management must be able to manage its business as effectively as possible in order to be able to communicate reliable information to the financial markets. To meet the expectations in terms of financial communication for a listed company, the management of the AMIDON site has a range of tools to control and master its activity. The goal of this approach is to have the most objective vision and be as close as possible to reality. The management control tools must provide a prospective vision to the controller. Three types of complementary devices are developed:

- The first dashboard (daily) makes it possible to analyze in the very short term the evolution of the incoming and outgoing data of the information system. It informs the controller about the order entries entered by the sales assistants, the production realized, the deliveries made and at what price. The indicators are tracked daily and announce the monthly trends. The data from this first dashboard is then entered into a second dashboard that will be sent to headquarters after each closing;

- The second dashboard, called Monthly, allows reporting. The controller will take stock of the situation at the end of the month and justify the differences at headquarters. Unlike the first dashboard, it is a reporting tool imposed by the group.

- The actions of progress called also Cost Take Out are imposed by the group and have for objectives to reduce the costs on all the posts and thus to improve the profitability of the various entities.

86These three dashboards are linked to one another and make it possible to control all the actions of the organization and their impact on the result and thus the satisfaction of the shareholders. These tools principally bring together financial indicators and are adapted to the group’s strategy. Unlike the BSC, they are defensive tools that favour a short-term vision of the organization.

MECATRONIC

87At MECATRONIC, the BSC project was interrupted. Several reasons explain this abandonment. Even if, due to a long-term financial structure, the company has weathered the financial crisis relatively well, the effects of which were beginning to be felt in France from 2008, it experienced significant difficulties during this period: its turnover decreased from 28 million € in 2008 to 14 million € in 2010; its workforce dropped by 22%. In addition, the years of strong growth that preceded turnaround seem to have led the company to neglect several critical variables:

“Between 2008 and 2009, we skipped quality for the benefit of growth; result: big trouble that cost us a lot”.

89Most of the executives on the Management Committee have been renewed (CFO, Human Resources Director, Production Manager). The CEO left the company and it was the Business Manager who took his place in the management of the company. In this context, the company has refocused on a few important customers with whom it has maintained a competitive position thanks to its responsiveness and innovation capabilities. For its new CEO (ex Business Manager), it is this context of change and uncertainty that explains in particular the abandonment of the BSC, for which he blames too much formalism:

“In time, if we had to redo the strategy map, it would be the same. In terms of formality, we have not crossed the threshold of monitoring indicators. Why? We are constantly making the wide disparity! (…) One of the defects of the BSC: the formalism. If the formalism must be too penalizing, in terms of energy, necessarily, it leads to the abandonment “(…) it is a methodology which corresponds well to an SME, but with a tool already in place to leave the indicators and a more shallow activity”.

91In the same vein, the CEO deplores the retrospective nature of the BSC, according to him, unsuitable in times of change:

“If it only serves to look in the rearview mirror—suffer and see—it does not mean anything».

93As a result, the BSC has been replaced by monthly direction tables that remain strongly inspired by the BSC:

“We use a management dashboard once a month where we find the axes of the BSC: Finance, Sales, Quality, HR”. We try to take stock once a month, as part of a management follow-up where the shareholder participates. I plan to do the same thing at a lower level, that is, at the level of the line leaders.”

2.2.2 – Lessons on favourable factors and barriers to learning

95It is appropriate at this stage to focus on the lessons that can be learned from this abandonment of the BSC with respect to the favourable factors and barriers to learning. Among the factors that played a positive role in both companies we may note in particular the very strong involvement of managers in an interactive dialogue with their employees around strategic issues. This fits more generally into the implementation of a participative management. It confirms Huber’s analyses (1991, p. 103), which emphasize the decisive role of social interactions in the interpretation process in particular. These observations are consistent with the recommendations of Kaplan and Norton which are based on the work of Simons (1995) and consider that the use of BSC as an interactive control lever is likely to favor double-loop learning. Our observations in the AMIDON and MECATRONIC companies are however different from this analysis showing that interactions are crucial at the design stage of the BSC. In other words, this would suggest that interactive control can occur during the design phase of a BSC and not only during its phase of use as a steering instrument. But, above all, the two cases studied enlighten us regarding the obstacles to learning born from the design of the BSC. Many authors (Argyris and Schön, 1978; Huber 1991; Bollecker 2002; Seo 2003) have identified several obstacles. Bollecker (2002) points in particular to the influence of human obstacles related to limits in cognitive abilities or the existence of defensive routines. These have been particularly highlighted since their first publications by Argyris and Schön (1978). Seo (2003) takes up this element, which he classifies as one of the emotional barriers to learning. To this he adds political barriers as well as barriers related to the imperatives of management control and this, in particular, in the context of capitalism and globalized economies. The abandonment of the BSC in both case studies alerts us to the risks that are detrimental to organizational learning. At AMIDON, it is the change of direction of the management control system towards financial control that is at the origin of the abandonment of the BSC: faced with shareholder pressures, the group strengthened its reporting and, in the unit studied, it replaced the BSC. The turnover of a party of executives, starting with the Director of the establishment, could also be a barrier to learning, especially in memorizing knowledge (Huber, 1991, p. 105). At MECATRONIC, the financial crisis experienced by the company and the departure of its main executives are at the origin of the abandonment of the BSC. New priorities were then defined in the direction of dashboards which, while taking over the architecture of the BSC, have a more operational vocation.

96Finally, despite these obstacles, if in both cases the BSC was abandoned, we note that it has inspired the various management control tools that replaced it. In both companies, it seems that a capitalization of learning, through the memorization of knowledge acquired during the design of the BSC, then occurred.

2.2.3 – A memorization of the knowledge acquired during the design of the BSC

97In both organizations, despite the departure of several executives and collaborators present during the BSC experience, it seems that there was a phase of memorization of the knowledge acquired during the design of the BSC.

98As Huber (1991, p. 105) points out, the storage of knowledge can involve the memorisation and archiving of information on the one hand and the computerization of organizational memory on the other. In both cases studied, the memorisation of information as a result of the design experience of the BSC was mainly reflected in the practices and representations of the actors. For Huber (1991) indeed, much of the organizational knowledge regarding how to do things is stored as standard operating procedures, routines and scripts. Managers routinely acquire and mentally store «soft» information. This is precisely what our observations tend to show at AMIDON and MECATRONIC.

99At AMIDON, even though the BSC was abandoned, the BSC experience has left a lasting impression. The latter has, as indicated by its CFO, «left a trace» to the extent that;

“It has created a new working method (…) it has enriched the other management tools by a multi-business approach leading to contradictory debates with a pooling of the knowledge of each to decide on appropriate actions”.

101This is confirmed by the Production Manager:

“The corporate culture remains impregnated by this collective approach (…) The cost reduction imposed today by the group that controls AMIDON gives rise to the constitution of working groups that reflect and decide at the same time on the objectives and actions to be taken”.

103According to him, this participative management logic is «directly inspired by the BSC approach». In addition, according to the CFO, «this teamwork systematically takes into account the performance axes of the BSC in the construction of new steering dashboards» which allows the actors to maintain the multidimensional vision of the BSC without being constrained «by its formatting, deemed too standard and therefore too rigid».

104However, the increasing mobilization of the actors in the activities related to the reporting tends today to reduce the periods of collective exchange. For example, according to a supervisor, the progress groups were removed and «everyone is working in his corner». The Quality Manager states that she «has less and less room for maneuver and that she «spends her time reporting». This recurrent reporting practice is likely to create new learning and challenge those emanating from the BSC.

105At MECATRONIC, if the BSC did not materialize in a management and monitoring chart of the indicators, the strategy map now constitutes a frame of reference for the CEO, who uses it as an instrument of dialogue with the shareholders and with his main collaborators:

“The strategy map helped me a lot to open up directions and make decisions but we did not keep the formalism of the BSC (…) I always communicate around the map—it allows me to set up blockages (…) The Philosophy is still there but formalism is no longer our goal (…) Today, the strategy map helps me a lot in the answers I need to give to employees. I share it with most of them (…) We discuss the map with the main shareholder—it allows us to discuss the business plan”.

107In addition, the four axes of the BSC structure the monthly management dashboards:

“Today we have monthly management dashboards in which we use almost all four axes of the BSC: Finance, Sales, Quality, Human Resources”.

109Another element also seems to have to be considered as learning coming into being during the BSC experiment: the development of an interactive approach to management control, insofar as the new top management encourages a participative dialogue, especially around the management dashboards:

“Once a month, we make a point at a Board of Directors meeting in which the shareholder participates. I would like to do the same thing, a notch below, at the level of the line leaders”

3 – Discussion

111The results of the study tend to show that, despite the abandonment of the BSC as a steering scorecard, a great deal of learning was conceived during its design phase. This is embodied both in the management style and in the new tools that have come to replace the BSC. We can learn several lessons about the critical role and characteristics of the design phase of the BSC and its strategy map (3.1). In both cases, the BSC has nevertheless been abandoned and this causes us to question the fragility of such a tool vis-a-vis the evolutions that a company can envisage. More fundamentally, there is questioning about the scope and limits of the BSC in its environment (3.2).

3.1 – The critical role and conditions of the design phase of the BSC and its strategy map

112The design phase of the BSC was instrumental in the ensuing learning. Several considerations are therefore important. In the first place, in both cases, the process was conducted in a participatory process within an executive committee expanded to include several Operational Managers. The design of the BSC proved to be a privileged moment of interactive control (Simons, 2015) during which the top-management of the company was involved in the debates and dialogue with its collaborators to conduct a reflection on the fundations of the strategy. Under these conditions, it appears that management control, through the design of a steering instrument such as the BSC, is able to create a key moment for strategic questioning. (Denis, 2003). The design of the BSC thus constitutes a special moment of strategic thinking, whereas it is traditionally recognized by the BSC as playing a leading role in strategic alignment. During this design phase of the BSC, the design of the strategy map proved decisive in that it structured the thinking of the actors involved and allowed them to collectively build a shared model of performance. This highlights the importance of the strategy map as a consubstantial instrument to the BSC, giving rise then to very interesting research perspectives on its nature and its ends. In particular, it would be interesting to examine how the strategy map can represent a translation of the business model of the company (Bénet et al., 2017); thus it could provide a representation of the theory of action and the premises of the strategy. The case of the MECATRONIC company where the strategy map was kept on despite the renunciation to use the BSC as a strategic management dashboard, is particularly enlightening in this regard.

113One of the limitations of our study undoubtedly rests on the fact that, due to its abandonment, we could not observe what would have been the role of the BSC during its exploitation phase as a steering tool. Again, it would have been interesting to examine its use as an interactive or diagnostic control lever and, in so doing, its role in strategic thinking and alignment. Despite this, several lessons are to be drawn from these two cases of abandonment of the BSC, particularly as regards the scope and the limits of the BSC in its environment.

3.2 – The scope and limits of the BSC in its environment

114The abandonment of the BSC in the two cases observed, while revealing several limitations of the model, questions us as to its fundamentals and provides us with several lines of research. In the first place, it is necessary to question what is really meant by the qualifier «balanced» scorecard, especially in a complex environment made of paradoxes. Other than the idea of balance, should we not consider that of equilibration? So would it not be more precise in the questions that take into account the paradoxes that we must look for in sources of learning (3.2.1)? Secondly, the abandonment of the BSC, especially in favour of reporting-oriented devices, questions us concerning the scope of a model, multidimensional and not exclusively financial, of performance, in a context of financialization of the economy. Should we not detect one of the paradoxes of contemporary management control in which multidimensional models of performance, based in particular on the recognition of the role of dynamic resources, skills or capabilities as intangible assets, come into tension with financial control models geared exclusively towards the creation of shareholder value? What can the learning born of the BSC represent then at the risk of a financial control (3.2.2)?

3.2.1 – Paradox, equilibration and learning